The Roller Coaster continued and on foot of the governmental stimulus packages, especially the expected sign off by President Trump of the US package, markets recovered some of the falls by Friday’s close. Despite this individual stock markets are still significantly down on their opening values of 1st January.

In Local CurrencyLastWeek Year toDate

UK Equities

6.5 %

-28.0 %

US Equities

10.3 %

-21.3 %

European Equities

7.1 %

-27.1 %

Japanese Equities

13.7 %

-15.2 %

Hong Kong Equities

3.0 %

-16.7 %

Emerging Market Equities

4.9 %

-24.4 %

As I write this update at 5.30 pm Irish time, the US Markets have added another 2% gain by this stage having been followed, somewhat meekly, by Europe. Australia has had its rebound today which was just mimicking that of the US and Europe on Friday which happened after hours for them. In the meantime, South Africa has finished in positive territory.

An Update on the Medical Situation

As the infection and mortality rates gather considerable pace, each country’s population has a heightened awareness of its own statistics. Nevertheless it’s worth thinking about the possible projected figures for the US by Dr Tony Fauci, especially in the light of its importance in the global economy. Dr Fauci is a leading American immunologist who, amongst other roles, serves as a member of the White House Coronavirus Task Force, and has been the one to correct many of President Trump’s “mis-statements” on Covid-19. In his estimate issued over the past weekend, the US could experience as many as 200,000 deaths due to the virus. The UK for its part, based on its similar lack of initial urgency in dealing with the problem, could possibly see over 40,000 deaths on a proportionate population calculation.

To put that into perspective the number of “Winter Flu” deaths in the US over a 6 month period would normally be circa 62,000 while the total deaths of US military in its 17 year involvement in the Vietnam conflict came to 58,318 (with over 150,000 wounded that required hospital care).

In terms of managing the impact of the virus if a large percentage of your population hasn’t had the virus, but you still have people who are infected that aren’t identified or isolated, then the virus will continue to spread. In the short term, lockdown measures will most likely increase in severity in most countries and even when the worst may have appeared to have passed in terms of infections and deaths, the need for social distancing will restrict the broad economy, especially in tourism and hospitality. All this means is that a “back to work” strategy is probably going to have to co-exist with distancing measures for far longer than anyone and any country might want.

What’s The Economic Impact, Now And Going Forward?

Oil has now fallen to $20 a barrel (partly due to a disagreement between OPEC and Russia about reducing production) and there is now a genuine concern that oil producers will run out of storage space for oil which cannot now be put to direct use due to closures of factories as well as global travel restrictions. The price of copper has fallen 27% year to date underlining, if it was ever needed, the major slowdown in global economic activity which is becoming more obvious as each day passes.

The US economy is now entering recession and with it all the other economies in the world. Initial jobless claims (a measure of the number of new filings to receive unemployment benefits) rose to 3.283 million for the week ending 21 March. The speed and magnitude of the move higher highlights how US businesses have had to let staff go in the face of the sudden coronavirus shutdown. There were, up to recently, 29 million people employed in travel, leisure and hospitality in the US, so the jobless numbers are going to soar in the next few days and weeks. Similar statistics are also appearing globally with similar proportionate numbers for each country. As a point of reference, the US unemployment rate in the 1930s Depression period was 25% of the workforce.

In recognising the gravity of the situation, the world’s central banks have been full-on in their support of liquidity and borrowing. This is, as was the case in the Global Financial Crisis, a knee jerk reaction to keep economies afloat where the cost of providing business supports and “helicopter money” has stored up problems for the long term as far as each country’s debt is concerned. The reality is that the cost of servicing all these debts is being handed down to several generations to come.

One of the major impacts from Covid-19 is likely to be in the area of globalisation. Goods made cheaply in the Far East may be re-categorised in terms of their importance to each country’s economy. It is likely that we will see less reliance on, in particular, the Chinese supply of goods as products are sourced closer to home or even made at home. This will bring, over the long term, changes in product innovation and employment as well as investment opportunities.

What Should Investors And Pension Holders Do Now?

Nobody knows how the economic situation will play out in the coming year and, by extension, we don’t know how stock markets will play out. The likely scenario of a major death rate in the US, while already known, is most likely not fully priced into markets. I expect that the fear and uncertainty of health at an individual level will most likely spill over, in the short term, to further falls in stockmarkets in the coming weeks. This, in itself, will lead to a major investing opportunity for those who have cash holdings or new monies awaiting investment either personally or in their pension funds.

Of course, some people who might have switched out a few weeks ago at the start of this recent problem may decide to wait for a lot longer before they dip their toe back in. In my experience when people switch into cash they often stay in cash for years afraid to come back into the market and therefore miss the upswing.

And finally, I repeat my previous advice :

If you are invested already, keep the faith even riding out a likely further downward movement of the next month. If you are considering selling out with a view to coming back in at a lower price, don’t! These markets move far too fast to be certain of not missing the upside when it comes.

If you are continuing to make, say, monthly contributions to your pension fund then the next few months will be an opportunity to invest at cheaper fund prices than in the past.

Clients who are nearing retirement, but who intend to avail of an Approved Retirement Fund option upon retirement, should remember that your investment horizon is not time limited to the date of your retirement. Rather it extends to the length of your lifespan and most likely that of your partner also, in which case maintaining equity exposure to achieve real returns above inflation over time continues to be as important as ever.

If you have funds held in cash or “new money” pending investment then prepare for an opportunity to invest at a heavy discount to the January 2020 market.

Block B, Maynooth Business Campus Maynooth, Co Kildare

Colm Nolan & Associates Limited is a private company limited by shares registered in Ireland 653843

https://www.waypoint.ie/wp-content/uploads/2020/04/Financials-scaled.jpg16962560Colm Nolanhttps://www.waypoint.ie/wp-content/uploads/2016/03/waypoint-logo.jpgColm Nolan2020-04-07 14:11:032020-04-07 14:11:06Covid-19 Update On Its Impact On Financial Markets 30 March 2020

With effect from 31 March 2020, following the Addendum of September 2019 to the Consumer Protection Code 2012 issued by the Central Bank of Ireland all financial intermediaries are required to ensure that, in providing a regulated activity to a consumer, if it pays or provides, or is paid or provided with, any fee, commission, other reward or remuneration in connection with the provision of that regulated activity to or by any person other than the Consumer or a person acting on behalf of the consumer, the fee, commission, other reward or remuneration:

Does not impair compliance with the regulated entity’s duty to act honestly, fairly and professionally

in the best interests of the consumer;

Does not impair compliance with the regulated entity’s obligation to satisfy the conflicts of interest requirements set out in Chapter 3 of this Code and, as applicable, the European Union (Insurance Distribution) Regulations 2018 (S.I. No. 229 of 2018);

Does not impair compliance with the regulated entity’s obligation to satisfy the suitability requirements set out in Chapter 5 of this Code and, as applicable, the European Union (Insurance Distribution) Regulations 2018 (S.I. No. 229 of 2018); and

In the case of a non-monetary benefit, is designed to enhance the quality of the service to the consumer.

Furthermore, a regulated entity must avoid conflicts of interest relating to the following:

Fees, commission, other rewards or remuneration linked to the achievement of targets that do not consider the consumer’s best interests e.g. targets relating to volume (including override commission) and bonus payments linked to business retention; and

Agreements under which the regulated entity receives a fee, commission, other reward or remuneration in the form of goods or services, in return for which it agrees to direct business through or in the way of another person.

Finally, an intermediary may use the description “independent” or use any other word or expression that is a derivative of, or similar to this term:

In its legal name, trading name or any other description of the intermediary, only where regulated activities provided by the intermediary are all provided on the basis of a fair analysis of the market; or

In any description of a regulated activity provided by the intermediary, only where that regulated activity is provided on the basis of a fair analysis of the market,

and,

in either of these circumstances, only where the intermediary does not accept and retain any fee, commission, other reward or remuneration where advice is provided in respect of regulated activities provided by the intermediary, other than:

A minor non-monetary benefit that includes, for example, attendance at a conference within the State, IT software or platforms, or hospitality of a reasonable de minimis value such as food and drink during a business meeting or conference; and

A fee paid by a consumer, or a person acting on behalf of a consumer to whom the advice is provided.

The background To This Particular Document

Pursuant to provision 4.58A of the Central Bank of Ireland’s September 2019 Addendum to the Consumer Protection Code, all intermediaries, must make available in their public offices, or on their website if they have one, a summary of the details of all arrangements for any fee, commission, other reward or remuneration provided to the intermediary which it has agreed with its product producers.

What is Commission?

For the purpose of this document, commission is the payment earned by the intermediary for work undertaken on behalf of both the provider and the consumer. The amount of commission is generally directly related to the premium or value of the products sold. There are different types of commission models:

Single commission model: where payment is made to the intermediary shortly after the sale is completed and is based on a percentage of the premium paid/amount invested/amount borrowed.

Trail/Renewal commission model: Further payments at intervals are paid throughout the life span of the product.

Indemnity Commission

Indemnity commission is the term used to describe a commission payment made before the commission is deemed to be ‘earned’. Indemnity commission may be subject to a clawback (see below) if the consumer lapses or cancels the product before the commission is deemed to be earned.

Life Assurance/Investments/Pension products

For Life Assurance products commission is divided into initial commission and renewal commission (related to premium), fund based or trail relating to accumulated fund.

Trail commission, fund based or renewal commission are all terms used for ongoing payments. Where an investment fund is being built up though an insurance-based investment product or a pension product, the increments may be based on a percentage of the value of the fund or the annual premium. For a single premium/lump sum product, the increment is generally based on the value of the fund.

Examples of products include Life Protection (for life assurance, specified illness insurance and income protection), Regular Premium Life Assurance Investments, Single Premium (lump sum) Insurance-based Investments, and Single Premium Pensions.

Clawback

Clawback is an obligation on the intermediary to repay unearned commission. Commission can be paid directly after a contract is concluded but is not deemed to be ‘earned’ until after a specified period of time. If the consumer cancels or withdraws from the financial product within the specified time, the intermediary must return commission to the product producer.

Other Fees, Administrative Costs/ Non-Monetary Benefits

A non-monetary benefit could include (but is not limited to):

Attendance at product provider seminars

Industry Educational Seminars

Use of Product Providers resources

Co-branded literature

Product Provider hospitality

Assistance with Advertising/Branding

Our Firm’s Approach to Fees & Commissions:

The Principal of Waypoint Financial Planning has been in the financial advisory business for over 30 years.

We have at all times provided our financial advisory and implementation services on a clear, transparent and client centred basis.

We have decided (as has most of the Irish financial advisory market) to remove references to “independent” from our market profile with effect from 31 March 2020. This is despite the fact that we have in recent years operated on a fee basis for a substantial portion of the client advice and implementation of personal financial products.

We do, however, continue to provide clients with a fair analysis of the products that may be applicable to their personal circumstances. As such where a financial product is arranged for a client we also continue to offer clients a choice of fee only or commission as a remuneration method for our services. This is offered to the client so that clients can choose what might best suit their own personal cashflow needs and personal taxation status.

Where commissions are chosen as the remuneration option by the client the pages which follow for each product provider set out the maximum commission terms available in respect of their products. In all cases with clients the commissions that we elect to charge are usually far lower than the maximum that could be paid. This is because it is our business policy to provide good value for clients by reducing as far as possible the charges that they implicitly encounter by mainly using “clean pricing” methodology in receiving commissions for lump sum pensions and investments and by using lower commission rates for recurring premium contracts.

Apart from the arrangement of insurance, pension and investment products we also offer a fee only service to clients in respect of:

Standalone financial planning which involves an independent assessment of their personal financial situation, and

Expert Witness Reports for use in legal cases involving financial products including Family Law cases or investment losses in general.

These fees are bespoke and are agreed in advance with the client before any work is undertaken.

List of Product Producer Agencies Held By Waypoint Financial Planning Limited

Product Provider

Life Assurance

Serious Illness

Income Protection

Investments

Pensions including PRSAs, ARFs & Annuities

Aviva Life & Pensions Ireland DAC

Yes

Yes

Yes

Yes

Yes

Conexim Advisors Limited

Yes

Yes

Independent Trustee Company Ltd

Yes

Yes

Irish Life Assurance plc

Yes

Yes

Yes

Yes

Yes

Mercer (Ireland) Limited

Yes

Yes

PortfolioMetrix Asset Management Ltd

Yes

Yes

Cantor Fitzgerald

Yes

Yes

Standard Life International DAC

Yes

Yes

Zurich Life Assurance plc

Yes

Yes

Yes

Yes

Yes

Aviva Life & Pensions Ireland DAC

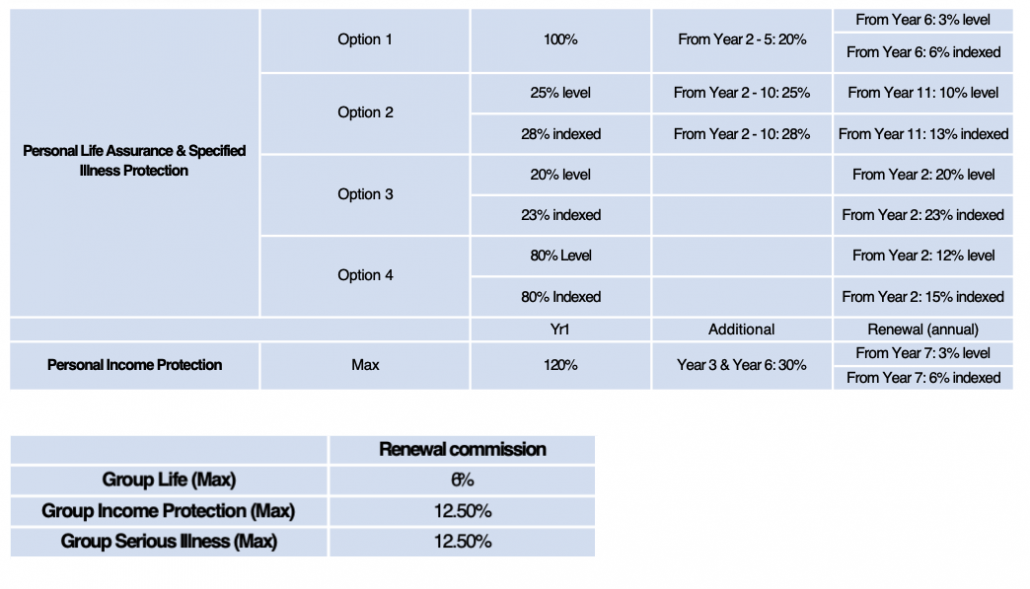

Waypoint Financial Planning deals with Aviva Life & Pensions DAC for protection covers of life assurance, specified illness insurance and income protection cover. We also use their investment and pensions (including PRSAs, Approved Retirement Funds, Buy Out Bonds and Annuities. Because of a merger with Friends First Life Assurance company in recent years they operate two sets of product each with their own commission structures.

Flexible Protection, Mortgage Protection Plan, Personal and Executive Pension Term Assurance

Period

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Rate Range

22% – 150%

3% – 22%

3% – 22%

3% – 22%

3% – 22%

3% – 22%

3% – 22%

Personal & Executive Income Protection & Wage Protector

Period

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Rate Range

30% – 200%

15% – 30%

15% – 30%

15% – 30%

15% – 30%

15% – 30%

15% – 30%

Heritage Aviva Product

Single Contribution Pension

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

1%

N/A

Single Contribution PRSA

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

4%

0.5%

N/A

Approved (Minimum) Retirement Funds

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

1%

N/A

Annuities

Initial

Trail

Bullet

Default

2%

N/A

N/A

Maximum

3%

N/A

N/A

Investment Bonds

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

1%

N/A

Investment Only

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

1%

1%

N/A

Regular Contribution Pension

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

15%

1%

40%

Regular Contribution PRSA

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

22.5%

0.5%

N/A

Savings Plan

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

15%

1%

N/A

Heritage Friends Product

Single Contribution Pension

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

0.75%

N/A

Single Contribution PRSA

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

7.5%

0.25%

N/A

Approved (Minimum) Retirement Funds

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

0.75%

N/A

Annuities

Initial

Trail

Bullet

Default

2%

N/A

N/A

Maximum

3%

N/A

N/A

Investment Bonds

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

4%

0.75%

N/A

Investment Only

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

5%

0.75%

N/A

Regular Contribution Pension

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

25%

0.75%

N/A

Regular Contribution PRSA

Initial

Trail

Bullet

Default

N/A

N/A

N/A

Maximum

17.5%

0.25%

N/A

Savings Plan

Initial

Trail

Bullet

Default

10%

N/A

N/A

Maximum

10%

0.75%

N/A

Group Life

Year 1

Year 2 onwards

Default

Flat commission of either 0% or 6%

0% or 6%

Maximum

6%

6%

Group Income Protection

Year 1

Year 2 onwards

Default

Flat commission of either 0% or 12.5%

0% or 12.5%

Maximum

12.5%

12.5%

Conexim Advisors Limited

Conexim Advisors Limited, is a custodial and stock dealing service that provides our clients with access to over 4,000 Funds from leading international fund managers as well as direct equity investments, fixed income securities and ETFs from all international markets. Conexim’s risk management, dealing, technical and platform administration services are provided in conjunction with Pershing Securities International Ltd. which is one of the largest established custodians in the Irish market for domestic investors.

While Waypoint Financial Planning no longer promotes itself as an independent financial advisor it should be noted that all fees and commissions processed on the Conexim Platform meet the definitions required to be considered ‘independent advice’ as defined under the MiFID II Regulations and the Consumer Protection Code 2012 (as amended).

Accounts on the Conexim Platform are legally and beneficially owned by the client in the case of Personal, Joint and Corporate Accounts, and beneficially owned by the client in the case of Trust based accounts (e.g. where the Trustee is the legal owner). Under Central Bank of Ireland guidance, in the case of single member pension schemes, the firm looks through to the underlying beneficiary in terms of conduct of business rules under MiFID II.

When a client opens an account on the Conexim Platform, the client states on the application form that: “The charges payable to my financial advisor which will be levied and deducted from my account are X%/€X Implementation, X%/€X Annual Charge. I hereby consent to the deduction of these charges from my account(s).”

As such, when our clients use the Conexim service they agree to a specified fee payable to this firm and not Conexim. They also agree for such fees to be deducted from their accounts and paid to our firm – i.e. Conexim is acting on the client’s behalf in paying the advisor, Waypoint Financial Planning, the fee from the client’s assets. The narrative on the client account when deductions are made, separate the Conexim Platform fee from the advisor fee, and they are recorded separately in the books and records of Conexim.

Conexim does not set the level of remuneration payable to this firm – it is agreed between the client and ourselves. Conexim therefore is collecting what is clearly identified as a standalone advisor charge and remitting it to our firm from the client account, based on a fee level agreed between ourselves and the client when using the Conexim Platform. This advice may be provided on an independent or non-independent advice basis by the advisor, but in no case does Conexim and Waypoint Financial Planning have a bundled fee arrangement.

For the avoidance of doubt, Conexim does not pay any remuneration to this firm for account referrals, persistency lapse rates, volume considerations, soft commissions or other metrics, and as there are no ‘lock in periods’ for investments on the Conexim Platform – there are no exit penalties, clawbacks or other detrimental fees levied on redemption or account closure.

Independent Trustee Company Ltd (ITC)

ITC is used by this firm in a trustee capacity to process individual PRSAs, Small Self-Administered Pensions, Buy Out Bonds and Approved (Minimum) Retirement Funds.

Accounts handled by ITC are legally and beneficially owned by the client in the case of PRSAs, Buy Out Bonds and Approved (Minimum) Retirement Accounts, and beneficially owned by the client in the case of Trust based accounts (e.g. where the Trustee is the legal owner). Under Central Bank of Ireland guidance, in the case of single member pension schemes, the firm looks through to the underlying beneficiary in terms of conduct of business rules under MiFID II.

When a client opens an account through ITC, the client may specifically instruct ITC to pay a specific charge to this firm which will be levied and deducted from their account i.e. ITC is acting on the client’s behalf in paying Waypoint Financial Planning the fee from the client’s assets. The narrative on the client account when deductions are made, separate the ITC fee from any fee paid this firm, and they are recorded separately in the books and records of ITC.

ITC does not set the level of remuneration payable to Waypoint Financial Planning – it is agreed between the client and this firm for advice related to one of the above products. Irrespective of whether this advice is provided on an independent or non-independent advice basis by any advisor, we can confirm that ITC and this firm do not have a bundled fee arrangement.

Irish Life Assurance plc

Mercer Ireland Limited (MIL)

Mercer Ireland Limited use the administration systems and commission terms of Zurich Life Assurance plc for the lump sum investment and pension products that they market to financial brokers.

Single Premium Product

Initial Commission

Fund Based Commission

Pension, including Buy Out BondsMax

5.50%

0.50%

PRSA (Standard) Max

5.50%

0.00%

PRSA (Non-Standard) Max

5.0%

0.50%

Approved (Minimum) Retirement Funds Max

5.0%

0.50%

PortfolioMetrix Asset Managers

While this firm has an agency with PortfolioMetrix Asset Managers for the purposes of using their discretionary investment management services we do not receive any commission or fee payments from them. Instead any fees that are chargeable on clients are agreed with clients directly and are chargeable by deduction through their account with Conexim Advisers.

Standard Life International Ltd

Single Contribution Products

Upfront Commission

Clawback Period

Fund Based Commission

Pension (Maximum)

5%

N/A

1%

PRSA (Maximum)

5%

N/A

0.5%

Approved (Minimum) Retirement Funds (Maximum)

Annuity (Maximum)

Investment Bonds (Maximum)

Regular Contribution Products

Initial Commission

Clawback Period

Renewal Commission

Fund Based Commission

Pension Front Loaded (Maximum)

1.25% X term to max of 25%

5 years

2%

1%

Pension Level (Maximum)

5%

N/A

5%

1%

PRSA (Maximum)

5%

N/A

5%

0.5%

Savings Plan – Funded by Initial Commission

0-15% payable as a lump sum after the first premium is paid

5 years

N/A

1%

Savings Plan – Premium Based

0% – 15%

N/A

N/A

N/a

Zurich Life Assurance plc

Single Contribution Products (Pensions, Investments)

Initial Commission

Fund Based Commission

Pension (Maximum)

5.50%

0.50%

PRSA (Standard) (Maximum)

5.50%

0.00%

PRSA (Non Standard) (Maximum)

5.0%

0.50%

Approved (Minimum) Retirement Fund (Maximum)

5.0%

0.50%

Annuity (Maximum)

3.0%

N/A

Investment Bonds (Maximum)

5.0%

0.50%

Trustee Investment Plans (Maximum)

5.0%

0.50%

Regular Contribution Products (Pensions, Savings)

Initial Commission

Renewal Commission

Fund Based Commission

Pension (Maximum)

20.0%

3.0% p.a.

0.50%

PRSA (Standard) Maximum

5.0%

5.0% p.a.

0.0%

PRSA (Non Standard) Maximum

5.0%

5.0% p.a.

0.50%

Savings Plan (Maximum)

10.0%%

1.0% p.a.

0.50%

Commission clawback:

Commission clawback applies over a 4 year period for all initial commission.

Commission clawback also applies over a 4 year period for any bullet commission noted.

Guaranteed Term Protection & Guaranteed Mortgage Protection

Year 1

Years 2 – 10

Years 11+

Maximum

100%

12%

3%

Commission clawback:

Commission paid in year 1 is earned over a 12 month period.

Guaranteed Whole of Life

Year 1

Years 2 – 5

Year 6+

Maximum

90%

18%

3%

Commission clawback:

Commission paid in year 1 is earned over a 12 month period.

Zurich Life Assurance plc

Group Life Cover

Year 1

Year 2

Year 3

Maximum

6.0%

6.0%

6.0%

Commission clawback:

Does not apply. Commission is paid as premiums are received.

Group Permanent Health Insurance & Group Serious Illness Cover

Year 1

Year 2

Year 3

Maximum

12.5%

12.5%

12.5%

Commission clawback:

Does not apply. Commission is paid as premiums are received.

For the PDF copy of this article, please click below.

The following is a summary of the tax changes announced by the Minister for Finance and Public Expenditure and Reform. Changes are effective from 1st January 2018 unless stated otherwise.

Income Tax

The tax credits and tax bands changes are in bold.

Tax Credit

Tax Credit

2017 €

2018 €

Single Person

1,650

1,650

Married or in a Civil Partnership

3,300

3,300

Employee Tax Credit

1,650

1,650

Earned Income Tax Credit Max

950

1,150

Widowed Person or Surviving Civil Partner (without qualifying child)

2,190

2,190

Single Person Child Carer Tax Credit

1,650

1,650

Incapacitated Child Credit Max

3,300

3,300

Blind Tax Credit: Single Person

Married or in a Civil Partnership – One Spouse or Civil Partner Blind Married or in a Civil Partnership – Both Spouses or Civil Partners Blind

1,650

1,650

3,300

1,650

1,650

3,300

Widowed Parent: Bereaved in 2017

Bereaved in 2016

Bereaved in 2015

Bereaved in 2014

Bereaved in 2013

Bereaved in 2012

– 3,600

3,150

2,700

2,250

1,800

3,600

3,150

2,700

2,250

1,800

–

Age Tax Credit:

Single or Widowed or Surviving Civil Partner

Married or in a Civil Partnership

245

490

245

490

Dependent Relative

70

70

Home Carer Tax Credit

1,100

1,200

Personal Circumstances

2017 €

2018 €

Single or Widowed or Surviving Civil Partner, without qualifying child

33,800 @ 20%

Balance @ 40%

34,550 @ 20%

Balance @ 40%

Single or Widowed or Surviving Civil Partner, qualifying for Single Person Child

Carer Credit

37,800 @ 20%

Balance @ 40%

38,550 @ 20%

Balance @ 40%

Married or in a Civil Partnership, one Spouse or Civil Partner with Income

42,800 @ 20%

Balance @ 40%

43,550 @ 20%

Balance @ 40%

Married or in a Civil Partnership, both Spouses or Civil Partners with Income

42,800 @ 20%

with increase of 24,800 max.

Balance @ 40%

43,550 @ 20%

with increase of

25,550 max.

Balance @ 40%

Tax Rates and Tax Bands

The exemption limits for persons aged 65 years and over remain unchanged:

Personal Circumstances

2017 €

2018 €

Single or Widowed or a Surviving Civil

Partner, 65 years of age & over

18,000

18,000

Married or in a Civil Partnership, 65 years of age &

over

36,000

36,000

The above exemption limits are increased by €575 for

each of the first two dependent children and by €830 for the third and subsequent children.

Marginal Relief may apply, subject to an income limit of twice the relevant exemption limit.

Mortgage Interest Relief

Relief is extended to existing recipients for a further three years on a tapered basis. Qualifying interest applies for each of the three years at the following rates:

2017

2018

2019

2020

Qualifying Interest

100%

75%

50%

25%

The interest ceilings are also reduced for each of the three years as follows

First time buyers

2017 €

2018 €

2019 €

2020 €

Single (unmarried or not in a civil partnership)

10,000

7,500

5,000

2,500

Married, in a civil partnership, widowed, or a surviving

civil partner

20,000

15,000

10,000

5,000

Non-first time buyers

2017 €

2018 €

2019 €

2020 €

Single (unmarried or not in a civil partnership)

3,000

2,250

1,500

750

Married, in a civil partnership, widowed, or a surviving

civil partner

6,000

4,500

3,000

1,500

No relief will be available from 1 January 2021.

Key Employment Engagement Programme (KEEP)

A new share option scheme will be introduced for employees of unquoted Small and Medium Enterprises with effect from 1st January 2018, subject to EU approval. Under this new scheme, any gain realised on the exercise of a qualifying share option, granted in the period

1st January 2018 to 31st December 2023, will be exempt from Income Tax, USC and PRSI, provided certain conditions are met.

Any gain on the subsequent disposal of the shares acquired under KEEP will be subject to Capital Gains Tax (CGT) in the normal way.

A new deduction is being introduced for pre-letting expenses of a revenue nature incurred on a property that has been vacant for a period of 12 months or more. The expenditure must be incurred within the 12 -month period before it is let as a rented residential premises.

A cap on allowable expenses of €5,000 per property will apply, and the relief will be subject to claw back if the property is withdrawn from the rental market within four years. The relief will be available for qualifying expenses incurred up to the end of 2021.

Universal Social Charge (USC)

Standard Rates of USC

USC Thresholds

2017

Rate

2018

Rate

Income up to

€12,012

0.5%

Income up to

€12,012

0.5%

Income from

€12,012 to

€18,772

2.5%

Income from

€12,012 to

€19,372

2%

Income from

€18,772 to

€70,044

5%

Income from

€19,372 to

€70,044

4.75%

Income above

€70,044

8%

Income above

€70,044

8%

Reduced Rates of USC

USC Thresholds

Individuals aged 70 years or over whose aggregate income for the year is €60,000 or less.

Individuals (aged under 70) who hold a full medical card whose aggregate income for the year is €60,000 or less.

2017

Rate

2018

Rate

Income up to

€12,012

0.5%

Income up to

€12,012

0.5%

Income above

€12,012

2.5%

Income above

€12,012

2%

Note 1. ‘Aggregate’ income for USC purposes does not include payments from the Dept. of Employment Affairs and Social Protection.

Note 2. A ‘GP only’ card is not considered a full medical card for USC purposes.

Exempt Categories remain unchanged.

2017

2018

Where an individual’s income for a year does not exceed €13,000

Where an individual’s income for a year does not exceed €13,000

All Dept. of Employment Affairs and Social Protection payments

All Dept. of Employment Affairs and Social Protection payments

Income already subjected to DIRT

Income already subjected to DIRT

3% Surcharge (non-PAYE income)

The surcharge of 3% on individuals who have non-PAYE income that exceeds €100,000 in a year remains unchanged.

PRSI Contribution Rates

PRSI

A1

S1

B1

Employee

4.0%

4.0%

0.9%*

Employer

10.75%

Nil

2.01%

B1 employee rate increases to 4% for income > €1,443 per week.

Value Added Tax (VAT)

Sunbed Services

The VAT rate on sunbed services will be increased from 13.5% to 23% with effect from 1 January 2018.

Charities

A compensation scheme is being introduced for charities which are unable to reclaim VAT on inputs. A capped amount will apply to the scheme, with pro-rata payments made where the amount claimed exceeds the amount available. Details of the scheme will be made available when complete.

Corporation Tax (CT)

Accelerated capital allowances for energy-efficient equipment

The accelerated capital allowances scheme for energy- efficient equipment is being extended for a further three years until 31st December 2020.

Capital allowances for intangible assets

A cap of 80% will apply in respect of the amount of capital allowances for an intangible asset, and any related interest expense, that may be deducted from relevant trading income arising from the intangible asset in an accounting period.

The cap applies in respect of expenditure incurred on intangible assets on or after 11th October 2017.

Details will be included in the Finance Bill.

Excise

Sugar Sweetened Drinks Tax (SSDT)

Subject to formal approval by the European Commission, the SSDT will be introduced, in April 2018. It will apply to first supplies in the State of water and juice based drinks with added sugar and a total sugar content of 5g or more per 100 millilitres.

Sugar content

(per 100 millilitres)

Rate

between 5g and 8g

20 c per litre

8g or more

30 c per litre

Drinks supplied in concentrated form will be assessed on the basis of the sugar content of the drink at the dilution level intended for consumption.

Capital Gains Tax (CGT)

CGT incentive for land and buildings held for minimum period of seven years

An amendment will be made to section 604A of the Taxes Consolidation Act 1997.

The amendment will provide that gains in respect of land or buildings that were acquired between 7 December 2011 and 31 December 2014 will be exempt from CGT if they are sold after four years and within seven years from the date they were acquired.

Capital Acquisitions Tax (CAT) / CGT

Leasing of agricultural land for solar energy production – CAT agricultural relief and CGT retirement relief

Amendments will be made to CAT agricultural relief and CGT retirement relief so that the leasing of agricultural land for the production of solar energy will not affect entitlement to the reliefs, where the area of the land which is leased for that purpose does not exceed 50% of the total area of the land concerned.

Further details will be included in the Finance Bill.

Exempt Class Thresholds

Despite expectations that the CAT thresholds would be increased, no change was announced in the Budget, so therefore the current thresholds will apply unchanged for 2018:

Threshold

Class

Applies to

Threshold

A

Children inheriting

from parent

€310,000

B

Inheriting from other

blood relatives

€32,500

C

Inheriting from

strangers

€16,250

The CAT rate stays the same at 33%.

Stamp Duty

Transfer or conveyances of non-residential property

The stamp duty on the purchase or transfer of non- residential property (including land) is increased from 2% to 6%. The new rate takes effect for conveyances or transfers of such property that are executed on or after

11 October 2017. Stamp duty is payable by the purchaser.

A stamp duty refund scheme will be introduced in relation to commercial land purchased for the development of housing. Developers will need to have commenced the relevant development within 30 months of the land purchase to qualify for the refund.

Consanguinity relief and agricultural property

The consanguinity (blood relative) rate of stamp duty was due to expire on 31 December 2017 but is to be extended for another three years. On or after 11 October 2017, it is to be charged at 1% of the consideration instead of being set at half the rate of stamp duty that applies to non-residential property. This means that the amount of stamp duty payable will remain unchanged.

This relief applies to transfers of agricultural property between certain blood relatives where the transferee is a young trained farmer who intends to farm the land or lease the land to someone who farms the land for a period of six years.

Benefit in Kind – electric cars & vans

From 1st January 2018 to 31st December 2018, where an employer provides an employee or director with an electric car or van, no taxable benefit will arise for them.

This exemption is limited to cars or vans which derive their motive power solely from electricity (no exemption is available in respect of hybrid cars or vans).

DIRT

Last year’s Budget provided for a phased reduction in the DIRT rate from 41% in 2016 to 33% by 2020:

DIRT Rates

2016 2017 2018 2019 2020

41% 39% 37% 35% 33%

In 2018 the DIRT rate will therefore fall to 37%.

Exit tax

The Budget speech made no mention of a reduction in the exit tax rate from its current 41%.

Social Welfare

State Pension increases by €5 pw from end March 2018

There is a general €5 pw increase to all Social Welfare pensions, including the State Pensions (Contributory and Non-Contributory) from the end of March 2018.

The new maximum State Pension (Contributory) from March 2018 will be €243.30 pw, or €12,695 pa.

Pensions

The Minister made no reference to changes in private pension tax reliefs or taxation of benefits despite significant discussions in recent weeks.

Income Tax Relief on Personal Contributions

Age attained during year

% of Net Relevant Earnings (max

€115,000)

Less than 30

15%

30 – 39

20%

40 – 49

25%

50 – 54

30%*

55 – 59

35%

60 and over

40%

The 30% limit above also applies to certain professional sportspeople (e.g. professional golfers) under 50 in relation to their income from their sports occupation.

Finance Bill 2017

The Finance Bill will be published on 19th October 2017.

From September to December every year, yachtsmen gather in the Canary Islands, awaiting the right trade winds, allowing them to begin their epic voyage across the Atlantic.

Destination; The islands of the Caribbean.

As the crew are busily stocking the yachts with supplies to last them on their three-week voyage, the skipper concentrates on the passage plan. Equipped with compass, dividers and chart plotter, he or she is responsible for ensuring they reach their goal – the islands of the Caribbean. The best course is carefully planned.

Waypoints

Along the chartered route, at various intervals, the skipper inserts essential reference points called Waypoints. These markers ensure the yacht is still on course to reach its destination and act as strategic points that direct it around navigational dangers.

Waypoints avert surprises and ensure the crew don’t wait until day 21 to discover that there is no land in sight.

With the sails set, and the trade winds from the east, crews set sail on their 2,700 nautical mile journey. All things going well, they should reach the Caribbean in about 21 days without any adjustment to their course.

However, the probability is they will encounter unforeseen events of some kind along the way; equipment may break or an Atlantic storm may blow up. Either way, the yacht may drift off course. The chart plotter will clearly show the error of the course. The Waypoint will identify just how far off course they have gone, and the skipper and crew will re-evaluate the course, and make the necessary adjustments.

Knowing your Destinations

Life is just like this. Our starting point is where we are now, and our destination is where we want to be in five, ten or twenty years time. But, we can’t know our destination unless we recognise what exactly are our goals, dreams and aspirations. Once we have done a certain amount of soul-searching, and established what it is we want out of life, and when, then we can set about planning our life journey. But, we also need Waypoints; points along the way where we stop and take stock to ensure we are on track.

Case Study

What surprises me most in my role as Financial Planner is when I ask a client what these goals are, very often they don’t know the answer. In the case of a married couple, though they may be blissfully happily married, they are surprised to discover that they each want different things. That’s ok, if both know and can plan for their goals.

Take for example a couple we recently met, let’s call them Joan and Martin. Both are in their 50’s, and together for nearly 15 years. Joan runs her own business and Martin is in the medical sector. They asked to meet us to discuss how best to invest €200,000 Martin had recently inherited from his parents’ estate.

Their first question to us was “Where should we invest?”. They expected us to launch into a spiel on the different investment products they should consider, and were more than a little surprised to be asked instead “What goals in your life would you love this money help you achieve?”

There was a long pause while each looked to the other. It transpired Joan actually wanted to expand her business with a long term view. Martin wanted to move to a house closer to the city, and was quite definite about retiring in the next five years.

Happily, through our comprehensive financial planning process, we examined their goals in greater detail, and prepared with them a comprehensive cash flow, tax ,retirement and investment strategy.

We helped then to devise their plan, provided a route to follow and they are now on track to achieve their combined individual goals. A review every year will ensure that they stay on track .

Their plan is not a rigid strait jacket but rather it has been designed to achieve their goals whilst ensuring they can maintain the lifestyle that they want in the meantime.

Life is not a dress rehearsal and whilst achieving their future goals is important to them, so too is enjoying the journey life has ahead of them.

Life is a Journey

So, what makes you happy? Where do you want to be in 10 years’ time? How is money important to you? Are you an entrepreneur itching to set up your own business? Or are you wasting time counting down the years to your retirement? Have you a dream of buying that house by the sea? Or an ambition to go back to university to get the degree you never go the opportunity to complete? The list is endless, but it is YOUR list.

To go through life without identifying your goals could be compared to a yacht drifting aimlessly in the ocean.

The Importance of Waypoint Financial Planning to Your Journey

At Waypoint Financial Planning we are uniquely positioned to help you identify and achieve your goals, while you get on with your life. We have the blend of professional skills to offer a personal approach and bespoke solutions. All our advisers are Certified Financial Planners with experience in taxation, business consultancy, investing, retirement planning and banking.

Your job is to decide upon your goals; our job will be to help you achieve them while enjoying life along the way.

https://www.waypoint.ie/wp-content/uploads/2016/03/Capture.jpg179274Colm Nolanhttps://www.waypoint.ie/wp-content/uploads/2016/03/waypoint-logo.jpgColm Nolan2016-03-21 09:27:432020-04-02 07:56:08The Importance of Waypoints on our Journey

Modern life is full of stresses and pressures but did you ever think that living too long could be one of them?

In the early part of the 20th century it would have been unusual for a person to live beyond their middle 50’s. (In 1910 the average life expectancy at birth was 54 years).

Now, as a result of improvements in infant care, immunisation, diet, health care and other scientific developments our life expectancy is increasing at the rate of 3.5 years in every 10. Within the next 50 years living to be 100 will be the norm.

So are we ready for this?

Hardly! We haven’t begun to consider or examine the potential implications whether social, economic or financial around living longer. One of the undoubted and obvious risks is the financial cost of living longer both for ourselves and our families but particularly where we need to enter some form of nursing home care.

Nursing home care is already costly with the Ombudsman reporting in November 2010 that some 23,000 of our over 65’s needed some form of long term nursing home care, representing 5% of that group. A subsequent report in October 2012 by Cardi estimated that an extra 2,833 people would need to avail of this care every year.

That’s a NET increase of c. 12% each year in the numbers needing long term nursing home care. And why are the figures not relatively static – well as any talking meerkat will tell you…”SIMPLES”. We’re all just living longer so it’s a natural consequence of longevity.

With an average annual cost of €55,000 per person each year, the current cost of Nursing Home care is c. €1.4 billion each year and is equivalent to 9% of the current health budget! And growing…… If you have a spare €½ million you could pay for yourself but what about your partner, or your Mum or your Dad and what about your Partner’s Mum or Dad? Now we’re up to €3million assuming nil medical inflation and they all only live for 10 years in need of nursing home care! Even if you’re receiving a Ministerial pension you’d find that difficult to manage!

So who’s going to pay this €1.4bn plus every year? At the moment the State subsidises the cost of nursing home care through direct subvention (for those who have inadequate income or means it meets 100% of the cost) or through a combination of direct supports and tax reliefs where the person and/or their family pay a part of the ongoing costs.

One such support comes in the form of the “Fair Deal Scheme” or to give it its correct title the Nursing Home Support Scheme. Under the “Fair Deal Scheme”, you’ve to give up 80% of your annual income and 7.5% of all assets every year while residing in a HSE approved Nursing Home. In return for this the State will (assuming you meet the care assessment and medical criteria) meet the balance of any cost.

Where you’re family home is one of the assets involved then the total annual contribution is capped at 3 years x 7.5% or a total of 22.5% of the value of your home.

The State also gives income tax relief on the costs we bear on certain health care. At the moment income tax relief is granted for the employment of a carer (limit is €50,000 each year) in a home setting or income tax relief at up to 41% in relation to nursing home costs we bear directly.

But with increasing numbers needing to avail of nursing home care and the high costs involves how much longer can we as a State continue to fund the NHSS and tax reliefs at their current levels?

Well if we have a reliable and broadly based tax base, then perhaps we could fund a scheme to meet the needs of a group of people who we’ve an obligation to look after and care for properly.

How do we build that base if approx. 22,000 of our young educated qualified people are emigrating to Australia and elsewhere each year thus rendering a substantial portion of our future tax base resident on the other side of the world? Unless we can retain these people or attract others to the country, our future demographic will be top heavy with dependant people with expensive healthcare needs.

There’s no philanthropic force out there writing cheques for nursing home or other health care costs. It’s the State – you and me, our children and grand-children who’ll have to pay this bill. So let’s start planning for the future rather than just arriving there.

After all there are now 3 certainties in life death, living longer and taxes….. Oh and by the way would anyone of tax paying age leaving the country please bring Granny and Granddad with you.

.

https://www.waypoint.ie/wp-content/uploads/2013/04/Colm-Nolan-Why-Use-Our-Service.jpg320450Colm Nolanhttps://www.waypoint.ie/wp-content/uploads/2016/03/waypoint-logo.jpgColm Nolan2015-10-23 16:23:162020-04-02 07:55:33Why is Grandad in Australia ? – Nursing Home Care – the mortgage of the future